What is an ETC? How investors can trade commodities on the exchange

Gold facts & figures Arnulf Hinkel – 16.07.2020

Find out what ETCs have in common with ETFs, how they differ and what to bear in mind when investing in commodities.

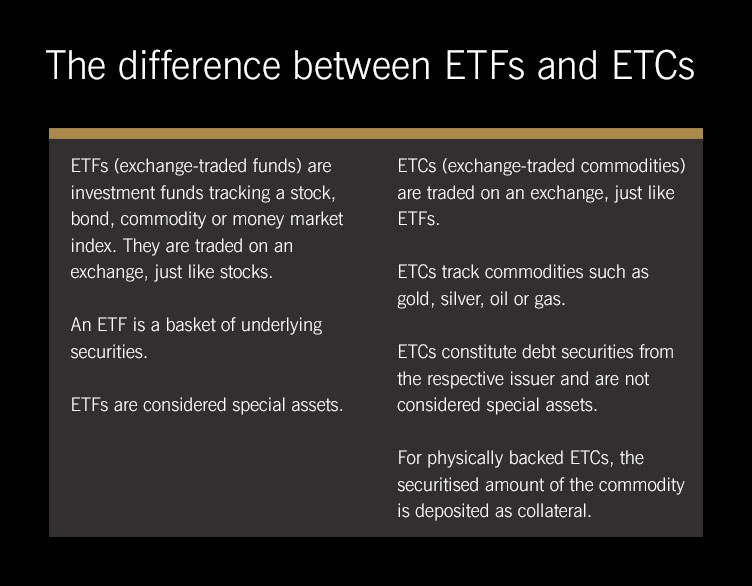

Most investors are familiar with ETFs (exchange-traded funds), but might not know all there is to know about ETCs (exchange-traded commodities). The two asset classes have a lot in common, but they also differ in many ways. First off, let’s look at what an ETC is and what opportunities it offers investors. ETCs are available for almost all types of commodities, which are typically sorted into the following categories: fossil fuels such as crude oil, natural gas or petrol; precious metals such as gold, silver, platinum and palladium; industrial metals such as copper, iron and aluminium; and finally, agricultural products such as cotton, wheat and coffee. The actual commodities can hardly be included into investors’ portfolios, with the exception of precious metals. Who would want to be responsible for the storage of large quantities of crude oil or cotton? That is where ETCs come in, allowing for easy and cost-effective commodities trading on the stock exchange. Generally speaking, ETCs follow the principle of ETFs. Investors can trade entire indices on the exchange just as flexibly, liquidly and cost-effectively as individual stocks, which is why ETFs are among the most popular forms of investment today, both among private and institutional investors.

Most investors are familiar with ETFs (exchange-traded funds), but might not know all there is to know about ETCs (exchange-traded commodities). The two asset classes have a lot in common, but they also differ in many ways. First off, let’s look at what an ETC is and what opportunities it offers investors. ETCs are available for almost all types of commodities, which are typically sorted into the following categories: fossil fuels such as crude oil, natural gas or petrol; precious metals such as gold, silver, platinum and palladium; industrial metals such as copper, iron and aluminium; and finally, agricultural products such as cotton, wheat and coffee. The actual commodities can hardly be included into investors’ portfolios, with the exception of precious metals. Who would want to be responsible for the storage of large quantities of crude oil or cotton? That is where ETCs come in, allowing for easy and cost-effective commodities trading on the stock exchange. Generally speaking, ETCs follow the principle of ETFs. Investors can trade entire indices on the exchange just as flexibly, liquidly and cost-effectively as individual stocks, which is why ETFs are among the most popular forms of investment today, both among private and institutional investors.

Image rights:© PantherMedia /ayo888

ETCs aren’t just “ETFs for commodities”

While an ETF tracks the performance of a single index, an ETC tracks the performance of a single commodity. The two asset classes thus appear to be quite similar. While this is true for the tradability of the two types of securities, ETFs and ETCs are fundamentally different from a legal perspective. While ETFs are considered investment funds, ETCs are debt securities from the respective issuers and valid for an unlimited period of time. The major difference is that in the event of insolvency of an issuer, investment funds are protected, while investors in debt securities can theoretically suffer a total loss of their investment. ETCs are collateralised to prevent this from happening. However, there are significant differences in both the type and quality of collateralisation, which investors should be aware of.

Three types of collateralisation for ETCs

The simplest and most transparent way to collateralise an ETC is to deposit 100 per cent of the respective commodity as collateral, which is relatively easy for precious metals such as gold. For each gold ETC unit, the issuer simply buys the corresponding amount of physical gold and deposits it safely. Some gold ETFs, such as Xetra-Gold, even offer buyers the right to delivery of the securitised amount of physical gold.

However, the situation is quite different for fossil fuels, industrial metals or agricultural products, requiring a different way of securitising – a physical deposit would be far too costly in terms of storage and transport. Still, for some securities such as oil ETCs, full collateralisation is possible via loan collateral or cash or securities deposits with very high credit ratings. This “swap-based” collateralisation usually requires daily review and adjustment, as the value of oil ETCs is constantly in flux.

A further swap-based form of collateralisation is through third-party coverage. However, ETCs thus secured are exposed to the risk of default of the third party, usually a bank or company.

ETCs on futures and the possibility of performance distortion

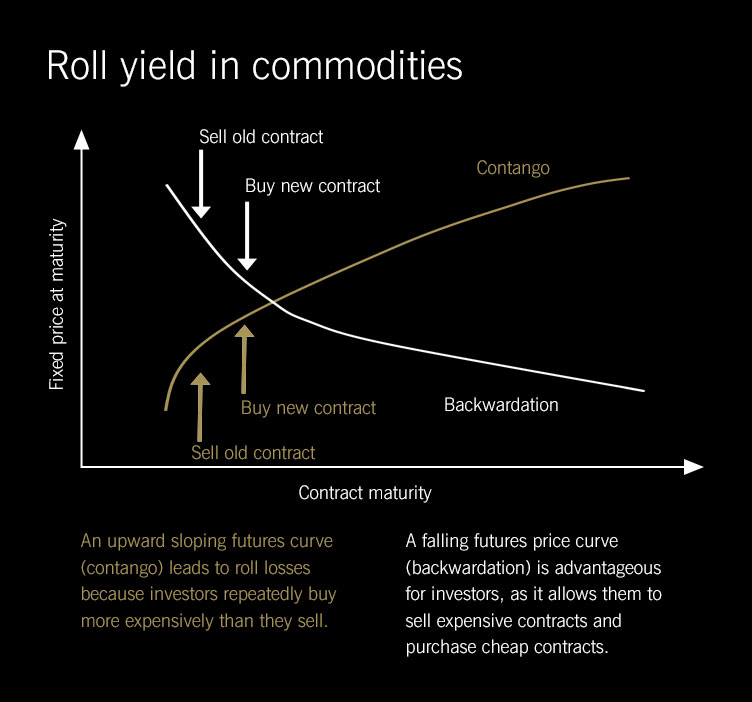

While ETCs on precious metals track the performance of the spot price, ETCs on oil, natural gas and agricultural commodities generally track the price development of the respective commodity future, i.e. the futures contract – the price development expected by commodity traders within a certain period, such as a quarter or a year. By their very nature, these futures contracts have a limited term and must be sold and replaced before they mature, or “rolled” over into a new future. Profits or losses depend on whether the newly purchased futures contract is cheaper or more expensive than the one sold. The price development patterns over time are called contango (when the futures price is above the spot price, and a loss is incurred) and backwardation (when the futures price is below the spot price, resulting in a profit). Both situations alter the performance of a futures-based ETC and result in the ETC no longer accurately reflecting the performance of the respective commodity.

What about commodity ETFs?

Given the amount of collateral required, why can’t commodities be traded on the exchange in ETFs, like indices? This is due to the EU directive UCITS (Undertaking for Collective Investment in Transferable Securities), requiring a minimum level of diversification for ETFs. In the EU, an ETF on a commodity index that includes various commodities is indeed possible; one that focuses on a single commodity, however, is not. In non-EU countries, where such ETFs are not traded in euros, an investment entails an unattractive exchange rate risk. Within the eurozone, investors are therefore much better off investing in ETCs.

It’s the total cost ratio that matters

Due to their high liquidity, trading ETFs and ETCs is cost-effective. But what about the running costs? Many investors are aware that active investment funds have significant management costs, which lower the return on investment. As index funds, ETFs passively track an existing market index or its performance. They have low management costs, reflected in a low total expense ratio (TER), i.e. the percentage amount of the sum of costs and fees associated with operating and managing a fund in its total assets. ETCs that are relatively easy to hedge with the commodity in question, such as precious metals like gold, also have a comparably low TER. As it only tracks the performance of a single underlying asset, which makes it similar to index funds, the respective TER is also similar. For example, the TER of both gold ETFs and gold ETCs are between 0.00 percent and 0.59 percent per year on average, which is significantly lower than those of investment funds, where they range between 1.5 and 2.5 percent annually.

Physical commodities vs. ETCs

Investors who want to trade commodities should first think about storage. With agricultural products, industrial metals or fossil fuels, this can quickly turn into a real challenge. For example, a private investor wishing to purchase 50,000 euros worth of UK Brent crude oil, which is commonly used in Europe, would have to find a storage facility for around 1,350 barrels containing 159 litres of crude oil each (as of July 2020). An investor who wants to invest in coffee would have similar problems: for the same sum, he would get around 30,000 kilos of coffee on the commodities market. In such cases, ETCs offer a cost-effective alternative. However, the type of collateralisation should be taken into account in order to assess the potential risk of default for third-party collateralisation. It is also important to consider whether the ETC in question represents the spot price or the forward price; in the latter case, there is a risk of performance distortion due to the effects of roll yield. For commodities with high storage costs or a strong dependence on weather or seasons in general, these distortions can be particularly noticeable and reduce potential profits in the form of unexpected additional costs.

The situation is different for precious metals: for example, the amount of gold that an investor could buy for 50,000 euros would fit into a pack of cigarettes. It would weigh less than one kilo (as of July 2020). Physical gold can thus easily be stored in larger quantities. However, this involves running costs for safekeeping, such as a safe deposit box or home security system. Also, the bid/offer spreads on gold bars and coins far exceed those of gold ETCs. Investors who want to add gold to their portfolio primarily as a stabilising element and inflation protection are much better off from a cost perspective with physically collateralised gold ETCs. When choosing a provider such as Xetra-Gold, where investors have the right to delivery of the securitised amount of physical gold, they can combine the benefits of exchange trading with physical ownership of the commodity.

Investors might also look for a liquidity reserve outside the financial system for the unlikely event of a complete collapse of the economic system. To have it readily available, they may choose to store gold bars or coins as an alternative means of payment. To do so, they must, however, bear the additional costs for purchase and safekeeping.

Interesting articles about gold

Interesting articles about gold

Youtube channel

Production of Umicore precious metal bars

Opening Bell Event zum 10-jährigen Bestehen von Xetra-Gold (German)

Gold als eigene Anlageklasse: Interview mit Steffen Orben (German)

Newsletter

Are you interested in receiving regular information on Xetra-Gold? Then subscribe to our monthly, free-of-charge newsletter to learn more about our gold holdings, upcoming events and to read our gold market outlook.

We are sorry that you consider to unregister from our newsletter. Are you missing out information? If yes, we are pleased to receive your feedback. Of course, you can always re-register at any later point of time.

Xetra-Gold Hotline

Do you have questions? We have the answers. Contact us here: 9 a.m.–6 p.m. CET

xetra-gold(at)deutsche-boerse.com

For press inquiries: media-relations(at)deutsche-boerse.com