Busting five gold investment myths

Gold facts & figures 23.11.2020

For thousands of years, mankind has appreciated gold for both its value and beauty. Over time, countless myths have developed surrounding the precious metal: that of the “Rhine gold” from the German Nibelungen saga, the vast gold riches of Atlantis, or the legend of King Midas, whose touch turned everything into gold, to name a few. Some surviving myths are not recognised as such, and many pertain to the characteristics and supposed disadvantages of gold as an investment. In this article, we will take a look at the most common gold myths, fact check them and assess their relevance for anyone wishing to invest in gold.

For thousands of years, mankind has appreciated gold for both its value and beauty. Over time, countless myths have developed surrounding the precious metal: that of the “Rhine gold” from the German Nibelungen saga, the vast gold riches of Atlantis, or the legend of King Midas, whose touch turned everything into gold, to name a few. Some surviving myths are not recognised as such, and many pertain to the characteristics and supposed disadvantages of gold as an investment. In this article, we will take a look at the most common gold myths, fact check them and assess their relevance for anyone wishing to invest in gold.

Myth no. 1: Gold is overvalued

Gold value has increased enormously in recent years. This year alone, the euro gold price has seen a rise to date of roughly 20 percent. Over the last five years, it has risen by 57 per cent. It is therefore no wonder that the precious metal is extremely popular among institutional as well as private investors. In view of the seemingly dizzying heights to which the gold price has risen both in euros and US dollars, an especially stubborn myth is celebrating a comeback: the claim that gold is both overpriced and overvalued.

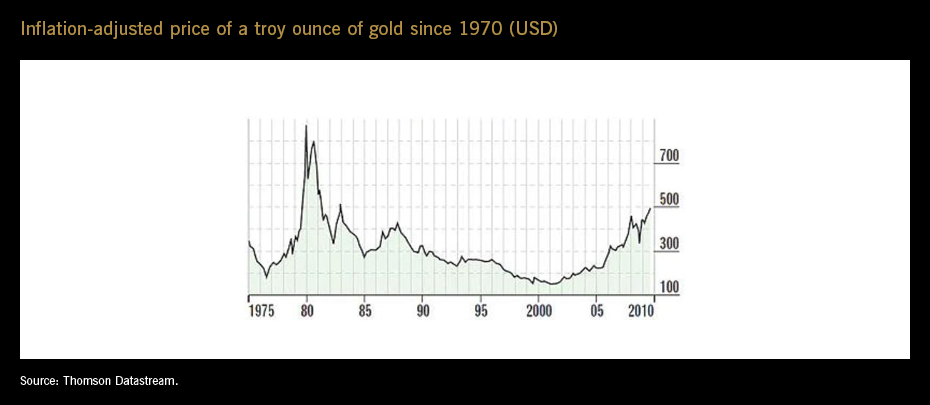

A superficial historical comparison of gold prices seems to confirm this myth, but is easily refuted upon closer analysis. The development of the gold price, adjusted for inflation, shows that one troy ounce of gold (approx. 31 grams) did in fact not reach its highest historical value when the US$2,000 mark was broken in early August 2020 but much earlier, in January 1980, when the troy ounce of gold stood at US$850 – i.e. US$2,300 adjusted for inflation. Empirically, there is thus still ample room for upward development.

Another approach to refute the myth is to look at the real value of gold. Has it gone up or down in value over the past millennia? If measured not in currency but simply in terms of purchasing power, the result is astounding. 2500 years ago, a troy ounce of gold could buy 350 loaves of bread, and today, it is about the same. Gold has thus maintained its purchasing power over the millennia, which also explains why it is often referred to as the hardest currency in the world and the best protection against inflation. Turn the tables and calculate the value of currencies in gold instead of the other way round to see just how stable gold is. Since early 2000 alone, the US dollar depreciated 82 per cent in terms of its purchasing power against gold, and the euro only marginally better off at 80.8 per cent. Gold has thus only seemingly becoming more expensive, when it is, in fact, currencies that are losing value. Even if the gold price is subject to fluctuations over time, its purchasing power is not, and neither is the value of the precious metal as a long-term investment and safe haven.

Myth no. 2: A non-interest-bearing investment, gold does not contribute to portfolio performance

This myth is half-true. While gold investors receive neither interest nor dividend pay-outs, gold can play a vital role in the performance of an investment portfolio. It does so due to its aforementioned purchasing power stability as well as via an increase in value. The latter is remarkable, from a historical perspective. With the abolishment of the gold standard in 1971, the gold price was no longer directly convertible into US dollars. Until then, one troy ounce of gold had been set at US$35. Since the end of the gold standard, the gold price has risen on average by more than 10 per cent annually against the US dollar – an excellent yield for an investment. It has, of course, not risen continuously over the past 49 years; there have always been phases in which it has moved sideways or downwards.

Gold, as part of an investment portfolio, is comparable to bonds of the highest credit rating, such as German government bonds. Neither investment entails the risk of total loss of the investment, but they do not generate interest earnings. In the current gold rally phase, the precious metal can also be compared to growth stocks, which allow for high price gains but do not pay out dividends.

Gold has a considerable advantage over most common types of investment, such as shares, bonds, ETFs, certificates and all forms of savings. This fact is also reflected in portfolio performance. Profits from the precious metal are not subject to withholding tax, provided the minimum holding period of one year is observed; withholding tax reduces returns by 25 percent.

Myth no. 3: Gold is highly volatile and therefore a purely speculative investment

Gold is a proven inflation hedge and serves as a reliable safe haven in times of crisis. Various studies have shown that it should be part of a well-diversified portfolio, as even in calm waters, a 5 per cent admixture has a stabilising effect and can contribute to performance. Gold as a long-term investment is therefore the exact opposite of a speculative object.

Quick profits with short-term gold investments are an entirely different story, as they can indeed prove to be highly speculative. The gold price is actually quite volatile due to a number of influencing factors. Gold price volatility is, however, by no means as high as that of other commodities (such as, for example, oil) and the precious metal also compares well with stocks. An analysis of various asset classes’ volatility between 2001 and 2019 by the US investor platform Morningstar Direct shows the volatility of gold was 21.52 per cent within that period. At the same time, industrialised countries’ stocks were only slightly less volatile at 19.66 per cent, while emerging market stocks had a significantly higher volatility than gold at 23.08 per cent.

Myth no. 4: Gold plays an insignificant role in the financial sector

Many investors believe that with the end of the gold standard, the precious metal’s importance in the global financial sector faded into oblivion. This is a misconception, as central banks have since continued to expand their holdings and store gold bars as foreign currency reserves. The World Gold Council’s latest figures (published in November 2020) show that 35,106 tonnes of gold are stored in central bank vaults around the world, proving that it remains a universal currency.

In defiance of the sceptics, gold is a popular investment. At the end of the third quarter of 2020, institutional and private investors worldwide held ETFs and ETCs physically backed by gold bars worth US$235.4 billion, and another 222.1 tonnes of physical gold are held by investors, a 49 per cent increase year-on-year and clear evidence that the importance of gold as an investment continues to grow.

Myth no. 5: Gold is an investment for times of crisis while stocks are always a good idea

Gold shines brightly in times of crisis, such as the global financial crisis in 2008 or the current coronavirus pandemic. But this does not mean that gold is not a popular and worthwhile investment in economically stable or booming phases. Economic growth and a rising GDP are, in fact, important drivers of gold demand. Increasing prosperity entails an increase in gold purchases, as proven by numerous examples from emerging markets and industrialised nations. In addition, an acclaimed quantitative analysis conducted by management consultants Mercer Germany, in which the profit and loss opportunities of a stock/bond portfolio were compared with those of a stock/bond/gold portfolio shows that the target return can be achieved both with and without the addition of gold. The risk of loss is, however, lower for a portfolio containing gold than for a pure equity/bond portfolio, with the assumed crisis probability of only 15 per cent.

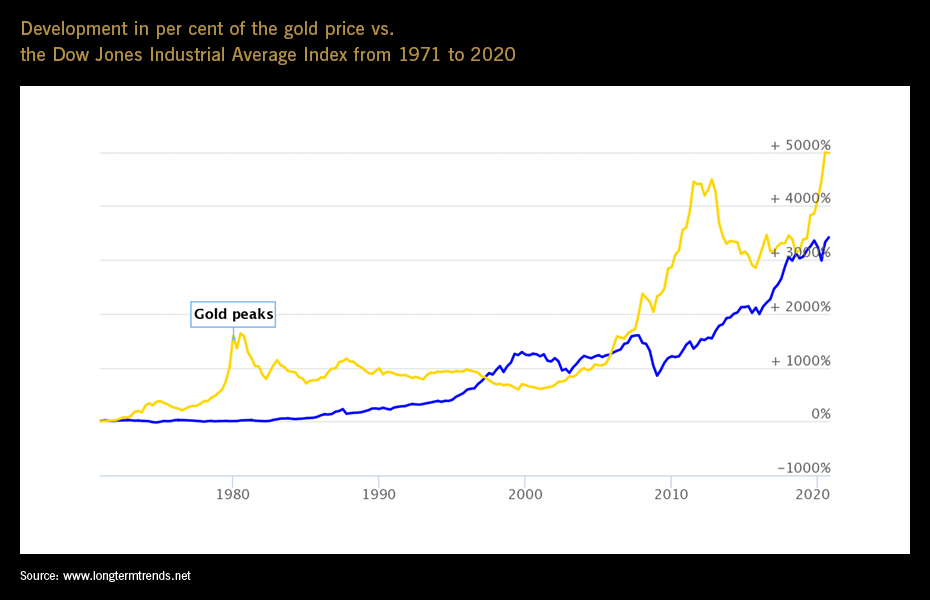

Direct comparison of the gold price development with that of the US Dow Jones Industrial Average Index (DJIA), one of the most important stock indices, also shows that the addition of gold to a portfolio can be worthwhile. Since the gold standard and thus the link between the gold price and the US dollar was abolished in 1971, the former has risen by more than 5,000 per cent until November 2020, while the DJIA Index has risen more moderately, by just above 3,400 per cent.

Conclusion: Gold myths are often just that – myths

Although there certainly is gold in the Rhine River, the old German Nibelungen saga is a legend. Many myths about gold are based on errors or exaggerated generalisations, where the exception is often misinterpreted as the rule. It is therefore for good reason that gold is popular among both professional and private investors, and not only in times of crisis.

Youtube channel

Opening Bell Event zum 10-jährigen Bestehen von Xetra-Gold (German)

Gold als eigene Anlageklasse: Interview mit Steffen Orben (German)

Newsletter

Are you interested in receiving regular information on Xetra-Gold? Then subscribe to our monthly, free-of-charge newsletter to learn more about our gold holdings, upcoming events and to read our gold market outlook.

We are sorry that you consider to unregister from our newsletter. Are you missing out information? If yes, we are pleased to receive your feedback. Of course, you can always re-register at any later point of time.

Xetra-Gold Hotline

Do you have questions? We have the answers. Contact us here: 9 a.m.–6 p.m. CET

xetra-gold(at)deutsche-boerse.com

For press inquiries: media-relations(at)deutsche-boerse.com